The Reaper Calls for Dignity

an investment report by Beyond (formerly Funeralbooker).

Short Thesis Summary

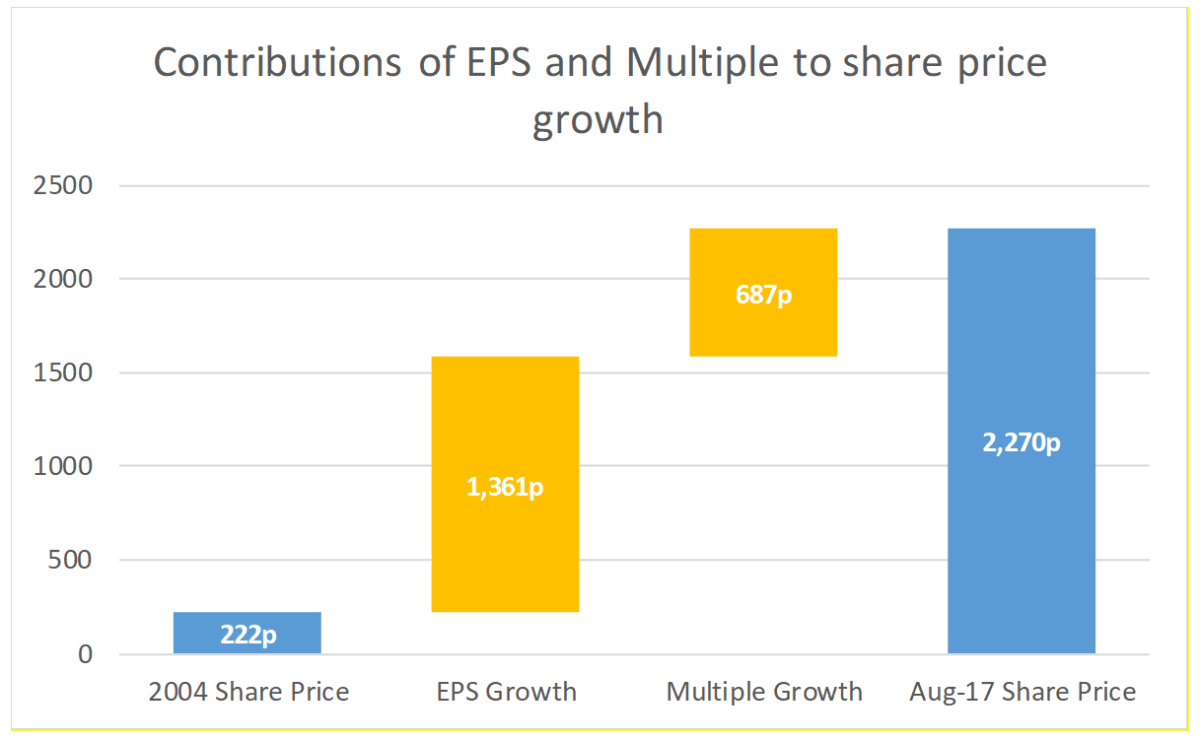

We believe that Dignity is currently valued based upon a view that EPS will continue to grow through a predictable increase in revenue and profits.

Between 2005 and 2016 (“the historical period”) the Company delivered:

- Revenue growth from £143 to £314 million (7.4% cagr)

- Operating profit growth from £42 to £98 million (8.1% cagr)

- EPS growth from 22.4p to 119.8p (cagr 16.5%)

There have been two drivers of this historical performance:

- a 53% increase in the number of branches (3.9% cagr); and

- an 81% increase in pricing (5.6% cagr)

The former is well publicised and reported on by Management. The latter, however, is not discussed publicly or reported on in annual reports. There are no KPIs reported relating to pricing.

To fully understand historical performance, and form a view on future prospects, it is necessary to analyse how both branch expansion and pricing have played their respective parts in Dignity’s growth story.

Our view on the historical contributions of these two drivers is that:

- Branch expansion has mainly functioned to keep customers steady and offset a collapse in branch productivity

- Dignity’s market share has been static at c.12% with customer numbers ranging from 62,300 to 73,500 as a function this static market share and a variable UK death rate

- Branch productivity, in terms of funerals performed per location per year, has collapsed by more than 30% from 129/year in 2005 to 87/year at H1 2017.

- Acquired locations typically provide around 150 funerals per year initially, offsetting customer losses elsewhere in the portfolio.

- Pricing has been used to provide constant top-line growth

- With customer numbers flat over the historical period, pricing has been used as a lever to provide revenue growth

- Prices increased every year between 2005 and H1 2017 from £1,699 to £3,153 at a cagr of 5.6%, in line with the growth within the Funeral Services segment cagr of 6.1%

Effectively, management have driven top line growth through large price increases across the existing portfolio, whilst offsetting decreasing customer numbers in the existing portfolio by acquiring new locations. The net result is that Dignity serves roughly the same number of customers each year but charges each of them a higher price.

We believe this is an unsustainable strategy with branch expansion and price increases both under threat.

The former, although not a focus of this report, logically ends at some point. The ability to ever expand branches without cannibalising existing locations or falling foul of competition concerns is not guaranteed. Dignity has twice chosen not to purchase the entirety of a target’s location portfolio, citing competition concerns[1].

With regards to the latter, price increases, Dignity has historically operated in an opaque market where customers have had little knowledge of what a fair price is. This is now changing rapidly with the advent of price comparison websites for the funeral industry. Within just a few clicks people can now see what funeral directors will charge them for a funeral.

Just as with air travel and hotels, the internet is democratising information and shifting power to the consumer. We anticipate that shifting buying/research online will see pricing pressure across the entire funeral market and result in flat/falling prices on an industry wide measure.

Within the industry, Dignity is the most exposed to any shift to price transparency and increased competition.

Following a decade of unremitting price increases, Dignity now operates at a totally disconnected pricing level to the rest of the UK market.

Based on customers through our site in the last year, a Dignity funeral costs 83% more than a funeral arranged through Funeralbooker.

Other estimates of this premium can be gained from Royal London 2016 research (45%), Ipsos Mori 2010 research (36%) and Sun Life 2016 research (32%).

This premium puts an extremely high incentive on funeral customers to “shop-around” and as such we believe Dignity will either have to reduce prices to compete or lose customers to competitors.

We have provided a financial model based on pricing reduction of 3.0% per annum between 2018 to 2021. This model produces a downside to analyst consensus estimates of EPS in 2018 and 2019 of 7.3% and 14.3% respectively.

REPORT STRUCTURE AND CONTENTS

Our report is structured as follows.

The first section is the summary of our argument.

Following this we have provided some background information on Dignity, the UK funeral market and the typical customer purchase cycle.

The main section of the reports begins with a look at Dignity’s historical performance. Within this, we will provide analysis around how the historical branch expansion strategy has been undertaken and its effects as well as analysis of how prices have changed historically.

We will then look at what constitutes a funeral, whether through Dignity or another provider and show that Dignity operates at a pricing level that is far in excess of market averages. In here, we will also talk about why we believe this pricing premium cannot be justified to customers.

Following this, we will detail why we believe Dignity will not be able to maintain this premium going forward, looking at the impact that price comparison websites will have on the funeral industry and examples of industries where this shift has played out previously.

We will close with a section on valuation.